In the USA, retirement income usually comes from more than one place. Most people get some money from Social Security, plus savings from a workplace plan like a 401(k) or pension, and sometimes an IRA. This guide explains these basics in simple language, so retirement numbers feel less confusing and calculators are easier to use.

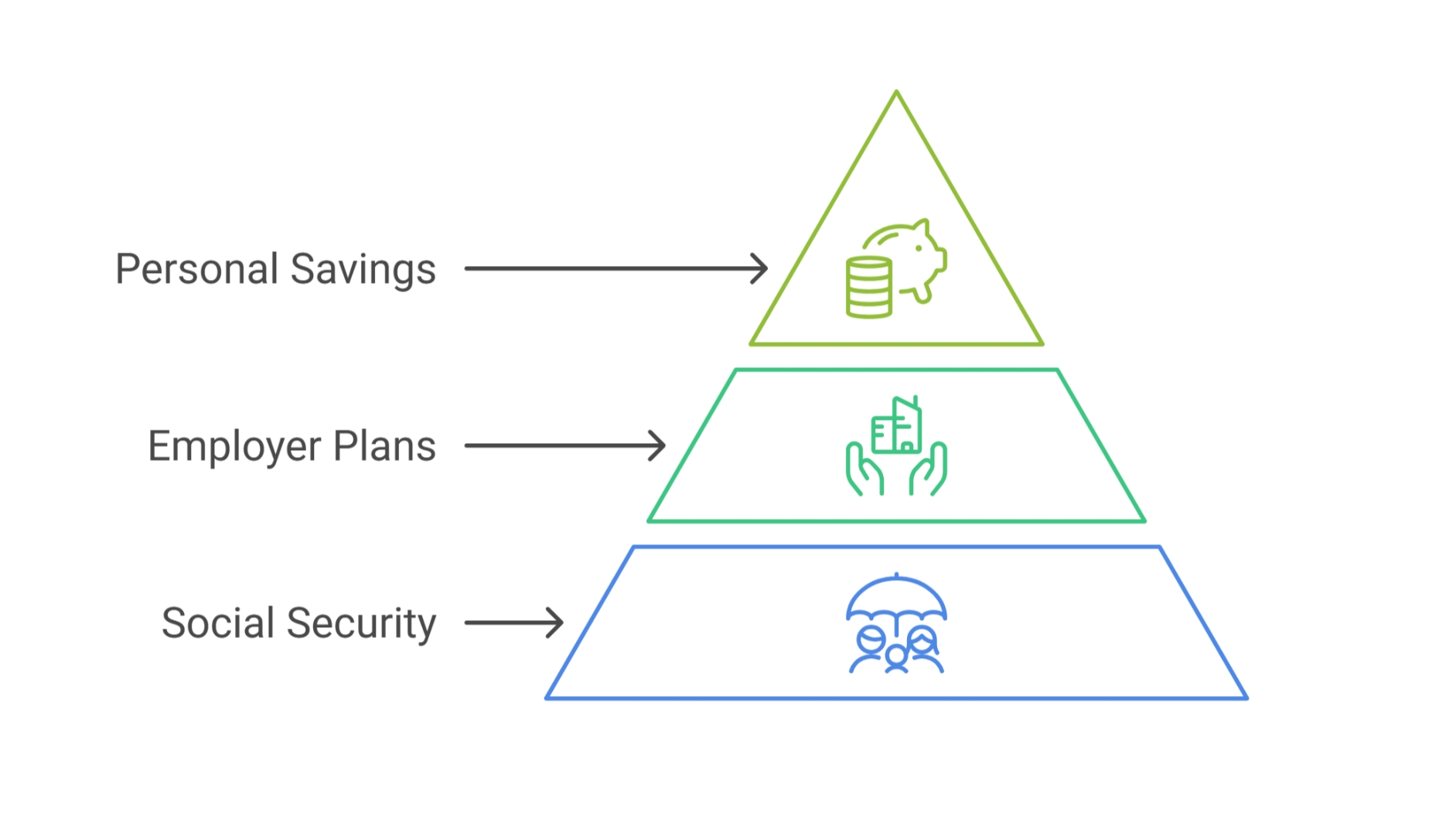

How the US Retirement System Is Structured

The US retirement system is not one single plan. It works like a 3-layer setup, where each layer can give you money after you stop working. Most people use more than one layer, so retirement income often comes from different places. When you understand these layers, retirement terms feel simpler and calculator results make more sense.

Layer 1 — Social Security (Government Income)

Social Security is the basic retirement income many people receive. While you work, money is taken from your paycheck as payroll tax. Later, when you retire, Social Security can pay you a monthly amount based on your work history and the age you start benefits. It usually covers only part of retirement income, so other savings often matter too.

Simple points to remember:

- Paid for through payroll tax while you work

- Monthly payment depends on earnings history and age

- Often gives a base amount, not full income

Layer 2 — Employer Retirement Plans (Work Plans)

Some retirement savings come through your job. This can be a pension or a 401(k), depending on the employer. A pension is usually based on a formula and may pay a steady income. A 401(k) builds a savings balance over time, based on what you contribute and how the account grows.

Simple points to remember:

- A pension usually pays income using a formula

- A 401(k) grows based on contributions and account growth

- Not every job offers the same type of retirement plan

Layer 3 — Personal Retirement Savings (Your Own Accounts)

This is retirement money you save on your own, outside of work. A common example is an IRA. You own the account, and it stays with you even if you change jobs. This layer helps add extra savings and can fill gaps if Social Security or a workplace plan is not enough.

Simple points to remember:

- You control the account (like an IRA)

- It stays with you even if you change jobs

- Helps add extra savings on top of other layers

Why These 3 Layers Matter

Most retirees do not rely on just one source of money. Social Security may give a base amount, workplace plans may add more, and personal savings can help cover what is left. This is why retirement calculators ask questions about your age, savings, and contributions. Each layer changes the final estimate.

Simple points to remember:

- Retirement income usually comes from multiple sources

- Calculator inputs reflect these different layers

- Understanding the layers makes results easier to read

What Is a Pension in the USA?

A pension is a retirement plan that an employer provides for workers. After a person retires, the pension can pay them regular income, usually every month. In many cases, these payments continue for life. This is why pensions are often seen as a traditional form of retirement income.

A pension is different from a 401(k) or IRA. It is not mainly based on how much money a worker saves in their own account. Instead, the retirement amount is usually worked out using a formula. That formula often looks at how long the person worked and how much they earned.

Key things to know:

- A pension is usually provided by an employer

- It can pay regular monthly income after retirement

- The amount is usually based on a formula, not just personal savings

How a Pension Usually Works

In most pension plans, the employer is responsible for managing the plan. That includes putting money into the plan and handling the investments. The worker usually does not choose the investments in the same way they might in a 401(k).

The amount a person receives in retirement is often based on two main things: years of service and salary history. Because of this, people who work longer for the same employer may receive higher pension income.

How it is often calculated:

- Years worked can increase the benefit amount

- Salary history is often part of the formula

- Payments are usually made every month in retirement

A Simple Pension Example

Here is a simple way to understand a pension formula. Let’s say a plan pays 1.5% of final salary for each year worked. If someone works for 30 years, they could receive about 45% of their final salary in retirement.

This is just a basic example, but it shows how pension income is often calculated. The longer a person works, the larger the pension benefit may become.

What this example shows:

- Pension formulas often use a percentage

- Longer service can lead to higher retirement income

- The final amount follows the plan’s rules

Are Pensions Still Common Today?

Pensions are not as common as they were in the past, especially in many private companies. Over time, many employers moved to 401(k) plans instead of traditional pensions. This means fewer private-sector workers now have pensions than before.

However, pensions are still common in some government and public-sector jobs. For example, teachers, police officers, firefighters, and other public workers may still have pension plans.

Why this matters:

- Pensions are now less common in much of the private sector

- Many employers use 401(k) plans instead

- Public-sector jobs are more likely to still offer pensions

Defined Benefit vs Defined Contribution Plans

In the USA, most retirement plans follow one of two main types. These are called defined benefit plans and defined contribution plans. The names may sound a little technical, but the basic idea is simple. One type focuses on a promised retirement income, and the other focuses on money being added to an account over time.

Understanding this difference makes pensions, 401(k)s, and IRAs much easier to understand.

Defined Benefit Plans

A defined benefit plan is a retirement plan that promises a set income after retirement. The amount is usually worked out using a formula. That formula often looks at things like salary and years of service. Traditional pensions are the best-known example of this type of plan.

In this model, the employer is mainly responsible for funding the plan and managing the investments. The worker usually knows how the benefit is calculated, but does not control how the money is invested.

Key things to know:

- A defined benefit plan promises retirement income based on a formula

- Traditional pensions usually follow this model

- The employer carries most of the financial responsibility

Defined Contribution Plans

A defined contribution plan is based on money being added to a retirement account over time. This type is used in plans like 401(k)s and IRAs. The final retirement amount depends on how much money goes into the account, how long it stays there, and how the account grows.

This means the final result is not fixed in advance. A person may retire with more or less money depending on contributions, time, and investment performance.

How this model works:

- Money is contributed into an account over time

- 401(k) plans and IRAs are common examples

- The final retirement amount is not guaranteed

The Main Difference in Simple Words

The easiest way to understand the difference is this: a defined benefit plan tells you more clearly what income you may receive later, while a defined contribution plan tells you more clearly how much money is being saved now. One is built around a benefit formula, and the other is built around account growth.

This is one of the main reasons pensions and 401(k)s work in different ways.

Quick takeaway:

- Defined benefit = focus on future retirement income

- Defined contribution = focus on money saved in the account

- This is why pensions and 401(k)s are not the same thing

Social Security Explained (Foundation Layer)

Social Security is a government program that helps provide income after retirement. While people are working, money is taken from their paycheck through payroll taxes. Later, that system can pay monthly benefits in retirement. For many Americans, Social Security is the starting layer of retirement income, but it is usually not the only source.

Social Security is mainly known for retirement benefits, but it also helps in other situations. It can support workers who become disabled and family members after a worker dies. This is why it plays a big role in the US retirement system. Still, it is not meant to fully replace a person’s salary after they stop working.

Key things to know:

- Social Security is funded through payroll taxes during working years

- It can pay monthly income after retirement

- It usually provides part of retirement income, not the full amount

What Social Security Provides

Social Security does more than just pay retirement income. It is also designed to support people if they cannot work because of a disability. In some cases, it can also help surviving family members. This makes Social Security a broader support system, not just a retirement payment.

What it can include:

- Retirement income

- Disability benefits

- Survivor benefits for family members

What Social Security Does Not Do

Social Security is helpful, but it has limits. It is not a personal savings account where your own money sits and grows over time. It is also not meant to fully replace your old paycheck. Because of this, many people also depend on pensions, 401(k)s, IRAs, or other savings during retirement.

What it does not cover:

- Full replacement of working income

- A personal savings account in your name

- A guaranteed retirement lifestyle

Why Social Security Is Called a Foundation Layer

Social Security is often called the foundation layer because it gives many retirees a basic monthly income. On average, it replaces about 30% to 40% of pre-retirement income. That helps explain why people often need other retirement savings too. Social Security is an important part of retirement income, but it usually works best as one part of a bigger system.

Why this matters:

- It often replaces only part of pre-retirement income

- Many people still need other retirement savings

- It works as a base layer in the overall retirement syste

Employer Retirement Plans in the USA

Many people in the USA get retirement benefits through their job. These are called employer retirement plans. The type of plan a person gets can depend on where they work, what kind of job they have, and whether the employer is in the public or private sector. This is one reason retirement benefits are not the same for everyone.

Some employers offer pensions, while others offer plans like a 401(k). In many cases, workplace retirement plans are an important part of retirement income, along with Social Security and personal savings.

Key things to know:

- Employer retirement plans come through a person’s job

- The type of plan can differ from one employer to another

- Workplace plans often make up an important part of retirement income

Traditional Pension Plans

A traditional pension plan follows the defined benefit model. This means the plan is designed to provide retirement income using a formula. The amount often depends on things like how many years a person worked and how much they earned. After retirement, the plan may pay regular monthly income.

In this type of plan, the employer usually manages the funding and investments. The worker receives the benefit based on the plan’s rules, rather than building the income in a personal account.

How traditional pensions work:

- They use a formula to calculate retirement income

- The employer manages the money and investments

- Payments are often made monthly after retirement

Where Traditional Pensions Are Still Common

Traditional pensions are not as common as they once were, especially in many private companies. Over time, many employers moved toward other retirement plans. Even so, pensions are still common in some types of work, especially in the public sector.

You are more likely to see pensions in jobs such as government, education, and public safety. These roles often still use pension systems as part of employee benefits.

Where they are often found:

- Government jobs

- Education roles, such as teachers and school staff

- Public safety jobs, such as police and firefighters

401(k) Plans

A 401(k) is a retirement savings plan offered by many private-sector employers. It lets employees save part of their salary for retirement. Often, employers add extra money to help grow the account faster. The total retirement income depends on how much is contributed and how the account grows over time.

Unlike pensions, a 401(k) does not guarantee a set monthly payment. Instead, your retirement income depends on the total amount in the account when you retire.

Key points to know:

- Employees contribute part of their paycheck to the 401(k)

- Employers may add matching contributions to boost savings

- Retirement income depends on the total account value over time

How Contributions Work

Money is automatically taken from the employee’s paycheck and added to the 401(k). Employers may match a percentage of contributions, which helps the account grow faster.

Quick takeaway:

- Employee contributions are regular and automatic

- Employer matching adds extra money to the account

- Matching helps your retirement savings grow faster

A Simple Example

If someone earns $60,000 a year and contributes 5% of their salary, they save $3,000 each year. If the employer matches 50%, that adds $1,500, for a total of $4,500 going into the account annually.

Over time, contributions and investment growth can make the account much larger, providing a bigger retirement income.

Why this matters:

- More contributions mean more money saved for retirement

- Employer matching increases total savings

- Investment growth over time affects the final retirement balance

Why 401(k) Plans Replaced Many Pensions

Over the past few decades, many private companies moved away from traditional pensions and started offering 401(k) plans instead. There are several reasons for this shift, mostly related to cost and flexibility.

With a 401(k), employers have lower long-term costs because they don’t have to guarantee a fixed monthly income. They also face less financial risk if employees live longer than expected. Finally, 401(k)s offer more flexibility for workers who change jobs more frequently, which is common in modern careers.

This change also shifted more responsibility onto employees. Now, workers must save and manage their own retirement accounts to ensure they have enough income later.

Key points to know:

- 401(k)s cost employers less over the long term

- They reduce the financial risk related to funding and employee longevity

- 401(k)s fit modern careers where people change jobs more often

What this means for employees:

- Workers now have more responsibility for saving for retirement

- Retirement income depends on contributions and investment growth

- Employees need to plan and save consistently to build enough retirement money

Who Typically Uses Each Type of Retirement Plan?

The type of retirement plan a person has often depends on the kind of job they work. Different jobs offer different retirement benefits, which is why retirement plans can vary a lot from one worker to another.

Many people also use more than one type of plan during their career. For example, they might get Social Security, a workplace plan, and also save in a personal retirement account.

Common Access Patterns

- Public sector workers – usually have traditional pensions, like government employees, teachers, and public safety workers

- Private sector employees – most often use 401(k) plans provided by their employer

- Self-employed individuals – rely mainly on personal retirement accounts like IRAs or solo 401(k)s

Key takeaway:

- Job type often determines which retirement plan is available

- Many people combine multiple plans for retirement

- Understanding your plan type helps you plan and save more effectively

Individual Retirement Accounts (IRA)

An IRA is a personal retirement savings account that you open on your own. It is not tied to your job, so you keep it even if you change employers. IRAs are often used to add extra savings on top of Social Security and workplace plans like pensions or 401(k)s.

With an IRA, individuals decide how much to contribute and manage their account within IRS rules. This gives more control and flexibility for long-term retirement planning.

Why IRAs Exist

- Help people save for retirement outside of work

- Provide options for those without employer retirement plans

- Give flexibility to grow savings over time

How IRAs Fit Into the Retirement System

- Supplement Social Security and employer-provided plans

- Offer tax advantages for long-term saving

- Stay with you even if you switch jobs

Retirement Age Rules in the USA

Age is an important factor in the US retirement system. Different retirement programs have different age rules, and your age is also a key input in retirement calculators. Knowing these rules helps you plan when to start receiving income and how much you may get.

Common Retirement Age Concepts

- Early retirement age – the age when you can start receiving benefits, but usually at a reduced amount

- Full retirement age – the age when you are eligible to receive full Social Security or pension benefits

- Required withdrawal ages – the age when you must start taking money out of certain accounts, like traditional IRAs or 401(k)s

Why Retirement Timing Affects Benefits

When it comes to retirement, the age you start collecting benefits matters. Most plans, including Social Security and pensions, adjust the amount you receive depending on when you begin. This is why timing your retirement can have a big impact on your income.

How Timing Changes Benefits

- Starting early – beginning benefits before full retirement age usually reduces monthly payments

- Starting at full retirement age – you receive the full planned benefit

- Delaying benefits – waiting past full retirement age can increase monthly payments

Tax Basics for Retirement Accounts

Retirement accounts in the USA have special tax rules to encourage long-term saving. How and when you pay taxes depends on the type of account you have. Understanding this helps you see how much money you may actually have when you retire.

How Taxes Apply to Retirement Savings

- Taxes when you contribute – some accounts let you put in money before paying income tax, while others use after-tax money

- Taxes when you withdraw – some accounts tax withdrawals in retirement, while others allow tax-free withdrawals

- Tax-deferred growth – money in many accounts can grow over time without being taxed each year

How These Retirement Components Work Together

Most people don’t rely on just one source of income in retirement. Instead, they usually combine multiple types of savings and benefits. Each component plays a different role to help cover living expenses after work. Understanding how these pieces fit together makes planning easier.

A Typical Retirement Income Mix

- Social Security – acts as a base layer, providing guaranteed income for everyday needs

- Employer plans – like pensions or 401(k)s, add extra income on top of Social Security

- Personal savings – such as IRAs or other accounts, provide flexibility and help cover any gaps

Example of How It Works

Imagine someone retires with the following mix:

- Social Security replaces 35% of pre-retirement income

- Employer savings cover another 25%

- Personal savings help cover the remaining 40%

This shows why combining different retirement sources is important to maintain a comfortable lifestyle.

How Pension and Retirement Calculators Use This Information

Pension and retirement calculators help you estimate your future retirement income. They do this by using information about how Social Security, employer plans, and personal savings work together. These tools make it easier to plan ahead and see how different choices may affect your retirement.

Common Inputs Used in Retirement Calculators

- Age and retirement timing – when you plan to start collecting benefits

- Contribution amounts – how much you and/or your employer save each year

- Existing savings – money already saved in 401(k)s, IRAs, or other accounts

What Calculator Results Represent

- Estimated income ranges – a general idea of monthly or yearly retirement income

- Scenario-based outcomes – shows how changing contributions or retirement age affects results

- General planning support – helps you understand if you may need extra savings

Important point:

- Calculator results are estimates, not guaranteed payments

- They help you plan better by showing possible outcomes based on your inputs

- Using them can guide your long-term saving decisions without promising exact results

Common Misunderstandings About the US Retirement System

Many people have misconceptions about retirement in the USA. These misunderstandings can lead to surprises later if planning is not done carefully. Learning how the system works helps you avoid mistakes and make more informed decisions.

Examples of Common Misunderstandings

- Relying only on Social Security – Social Security usually covers only part of retirement income, not everything

- Confusing pensions with 401(k) plans – pensions promise a set income, while 401(k)s depend on contributions and growth

- Treating calculator results as exact predictions – calculators provide estimates, not guaranteed outcomes

- Assuming you can retire at any age with full benefits – early retirement may reduce monthly payments

- Ignoring taxes on retirement accounts – different accounts have different tax rules that affect how much you actually receive

- Believing all jobs offer retirement plans – not every employer provides a pension or 401(k), so access can vary

- Thinking retirement savings start later automatically – retirement planning usually depends on consistent contributions over time

- Assuming all retirement accounts work the same way – different accounts (pensions, 401(k)s, IRAs) follow different rules and structures

Conclusion:

The US retirement system is made up of different parts working together, rather than just one plan. Each piece of Social Security, pensions, 401(k)s, and IRAs has its own role in helping people prepare for retirement.

Knowing how these components work together helps you understand retirement estimates better and use pension or retirement calculators more confidently. This understanding is meant to inform and guide planning, not to provide personal financial advice or guarantees.